3 Ways Life Insurance Can Save You Money

by Jamie Hale, Co-Founder and CEO

I know firsthand how life insurance can change lives because my father passed away when I was 11. The basic policy he had in place gave us financial stability when we were going through our hardest emotional season and allowed us to stay in our community and receive their love and support. That is an important part of his legacy.

You’re probably thinking “how can life insurance actually save me money?” Let me break it down for you.

1. Why do people even need life insurance?

If anyone (a partner, children, or elderly parents) depends on you for financial support, then purchasing life insurance can provide them with a financial safety net if something happens to you. It’s also a good idea if you have any debt co-signed, such as student loans or a mortgage.

2. Life insurance can be affordable and helps protects your family as you pay down debt or save for your kid’s college.

A healthy 30-year-old woman could get $100,000 of term coverage for as low $9-10 per month. That could help get a child through college or pay-off student loans. Term life can also be more affordable than whole life (3-10x less by some estimates) for the same level of coverage. This allows people to buy term and consider investing the rest – where you get life insurance coverage, then take the money you would have spent on another, more expensive, life insurance product and apply it elsewhere. Many people wonder about the best term life insurance plan, which is where “laddering” comes in.

3. If you “ladder” your term life insurance, you can spend only what is absolutely necessary

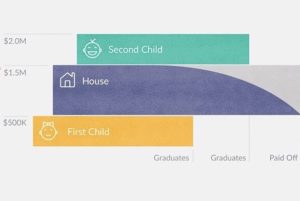

Life insurance can cover the most important things in your life – your partner, your children, your home, your parents. But you don’t suddenly wake up one day with three kids, a four-bedroom house and aging parents. These changes happen over time.

Planning out the most efficient use of your life insurance dollars can save you money in the long run.

Here’s an example:

If you get a modest 30-year term policy when you are young and healthy, odds are you will secure a lower rate, locking in a low monthly payment for 30 years. This means when you are older, have a mortgage, and find yourself in the “young kids / aging parents” sandwich, you’ll still be paying that low rate. The difference that you would have spent (had you bought a policy decades later when you were in the thick of parenting and mortgage debt) you can allocate to other, uses or investment strategies.

Now the laddering part. If you need to decrease coverage because your mortgage is decreasing, or your children are grown, you can make those changes as life happens and pay less each month. If you need more coverage, you can apply for more to ladder up.

At Ladder, we’ve calculated that customers can save up to 40% on their life insurance costs by “laddering down”, and we have an easy example on our blog that really brings this to life.

If laddering is of interest to you, make sure you work with a company that doesn’t charge policy fees and penalties.

Your future self will thank you.